Optimising market opportunities for lamb this summer

The GB lamb market has been on fire recently with prices continuing to surpass the usual market highs over easter and Ramadan. Strong demand was experienced over the Muslim festival of Ramadan and Eid, the trade rose 110p over a three-week period peaking the week after Eid. This is a strong reminder of the importance of this festival on the British lamb market.

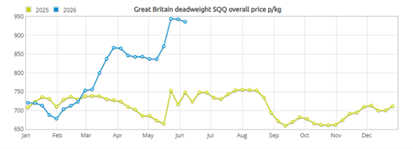

Deadweight price for a 2026 born R3L peaking at 942.5 ppkg, 189.3 ppkg ahead of last year (AHDB w/e 23/6/25). This has eased slightly due to more new season lambs coming onto the market to sit at 935.7 ppkg (w/e 6/6/26). Liveweight price is also telling a similar story with prices peaking at an average of 465.52 (w/e 6/6/26) a 24.6% increase year on year.

Prices have been driven by several factors including further contractions in the UK flock. Latest figures published by AHDB in April show a continued decline in the national flock, the data shows a 2.1% reduction in the UK flock on the previous year. Last year’s drought during spring and summer months coupled with disease (Schmallenberg and Bluetongue) has reduced lamb numbers, impacting the supply earlier in year. Supply was impacted earlier on in Q1 with a strong number of hoggs carried over into Q1 this year, supply has since trickled off as into Q2. Numbers are now picking up again with the arrival of this year’s lamb crop to the market.

Demand has remained strong driven by exports into the EU with Q1 exports up 18% year on year and the EU commission estimating a 5% increase in imports in the EU over the next year, the picture here is positive provided UK supply allows. Domestic demand is more of a steady picture with lamb spend increased, but overall volumes slightly down. Imports into the UK are remaining steady with Australia largely offsetting the reduction in lamb coming across from New Zealand. Flock decline is not confined to the UK as worldwide inventories and projections highlight declines. Australia is predicting a 2.7% decline in their national flock on the year according to MLA (Meat & Livestock Australia). They also predict to slaughter 11% less lambs on the year.

The strength of the current market brings with it opportunities for producers to capitalise. The first place to start is by monitoring this year’s lamb flock to assess if they on track to hit the market by their target date. We can then identify potential areas to either optimise growth to hit the market sooner or where potential cost savings may be made in to order to improve margin and therefore potentially profitability during a strong market.

Nutrition will undoubtedly play a key role in both these targets, being a key driver for performance.

Nutritional opportunities to optimise gain:

- Increasing gain from grass – is grass quality and quantity available sufficient to keep up with demand and optimise performance, could grazing strategy be improved?

- Optimising home-grown inputs – silage/hay quality, forage cropping for overwintering hoggs, other feed resources available on farm such as brassicas, cereals, legumes etc.

- Consider creep feeding to get lambs away quicker especially as grazing availability reduces later in the season.

- Trace element status – are lambs in an optimum trace element status to support performance?

Other considerations

- Worm control strategy.

- Stocking density – is the stocking density correct for grazing available?

- Weaning date/protocol to reduce check while optimising performance of both the lamb and ewe.

Lorna Shaw, Ruminant Nutritionist, Lorna.Shaw@sac.co.uk

Posted by SAC Consulting on 16/06/2026