Sheep Market Commentary and Outlook

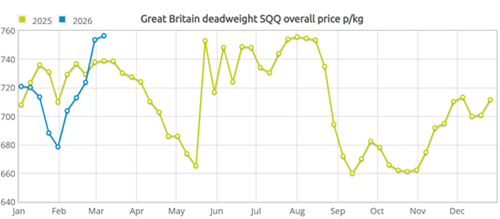

This year, deadweight prices initially declined, dropping to a low of 678.7 p/kg (w/c 31 Jan) which unusually coincided with a drop in supply. Despite this, prices remained strong compared to 2025. February has recorded recovery with prices increasing again just marginally behind 2025 prices throughout the month. This increase in demand coincided with the start of Ramadan on 17 February. Religious festivals are undoubtedly a key driver for our sheep market with 30% of UK sheep meat consumed going to 6.5% of the population in the UK (AHDB, 2024). This demand has led to deadweight prices peaking this year above the 2025 high at 765.5ppkg (w/c 7 March).

From mid-February onwards we have seen an increase in the number of old season lambs culled compared to this time last year (+30.7%). Perhaps a response to demand but also an indication of an increased number of lambs finishing later this season; maybe not a surprise given drought conditions and forage shortages in many areas in 2025 which will have undoubtedly impacted on the early growth rate of lambs.

In their latest market output, AHDB has estimated a 1% increase in lambs carried over into 2026 from last year. Liveweight has followed a very similar trend with standard to medium hoggs (32.1-45.5kg LW) gaining a stronger price per kg highlighting a demand for well finishing lambs.

Source: AHDB, 2026

The cast ewe trade remains strong and is currently in line with averages seen this time last year.

2026 so far has also seen changes to grading and reporting for lambs with standardisation of dressing specifications and weighing methods, which should improve transparency and price reporting accuracy. The introduction of a new “S” (Superior) grade which lies above the “E” (Excellent) grade will help better reflect carcase quality. This has also meant a change to reporting moving forward due to a requirement for all abattoirs to report price.

Price information will now be published for prime sheep falling within the SQQ weight band (12 kg to 21.5 kg) and dressed to UK-standard specification (kidney knobs, channel fat and diaphragm skirt removed). A positive step to improve accuracy and quality of sheep industry market data moving forward.

The global market

Sheep numbers and lamb sales are continuing to constrict in Australia with slaughter numbers of both sheep and lamb for week commencing 6 March down 22% year on year. This has been predominantly driven by poor seasonal conditions. The flock rebuild expected to start in 2026 is likely to be gradual due to the smaller breeding flock and poorer scans. However, we are likely to see an increase in Australian supply over time coupled with an increase in efficiency with average carcass weights increasing by around 1kg over the last 3 years. Demonstrating a move to producing more from less.

In 2025, New Zealand recorded a 2% increase in lamb numbers compared with 2024, but remains a low threat compared to historic years due to their long-term flock contraction with breeding number continuing to see a decline.

Both countries are target growth markets for Asia and the US. With the US remaining a key target market. However imposed tariffs are making this slightly more challenging despite the reduction from 15% to 10% being welcomed. With growing unrest this could lead in an increase in Australian lamb coming towards the UK which may pose a long-term risk for the UK domestic price.

The EU however remains a key location for our UK lamb with export volumes increasing last year by 9% despite higher prices with key markets being France, Germany, Belgium, Italy and the Netherlands.

Market outlook

Tight domestic and EU supply, resilient export demand particularly from the EU, and constrained global production provide a solid potential market going into the rest of the year. However, global competition and current events leading to potential political unrest mean volatility remains a risk in the longer term.

Lorna Shaw, Ruminant Nutritionist, Lorna.Shaw@sac.co.uk

Posted by SAC Consulting on 16/03/2026