Autumn Budget: Key Implications for Agricultural Businesses

The 2025 Budget was outlined by the Labour Chancellor, Rachel Reeves, on 26 November. This year’s Budget focuses on raising additional revenue and restoring fiscal sustainability — effectively attempting to “balance the books” through increased taxation rather than major spending cuts.

Although the manifesto commitment not to raise Income Tax, National Insurance or VAT has technically been maintained, the overall package shifts more pressure onto businesses, including agricultural employers. Most individuals and businesses are expected to pay more tax over the forecast period. Further clarity will follow in the Scottish Budget on 13 January, particularly on Income Tax and property-related measures.

Underlying this strategy is the central challenge highlighted by the Office for Budget Responsibility (OBR): weaker projected productivity. The OBR has downgraded its medium-term productivity forecast, which on its own reduces projected tax receipts by around £16bn in 2029-30.

GDP growth in the forecast period averages about 1.5% a year, while inflation is expected to run at a higher level, only returning to the 2% target in 2027. The government is still forecast to meet its fiscal rules — but only because this budget delivers substantial increases in tax revenue, with tax changes totalling about £26bn per year by 2029-30.

Notably, no substantial growth plan accompanied the budget. The OBR confirmed that none of the 85 policy measures announced materially affect the UK’s medium-term growth path.

Summary of key changes that affect agricultural businesses

Economic Backdrop

- OBR now assumes lower productivity and only modest medium-term growth (down from 1.3% to 1%), despite higher public investment.

- Inflation is forecast to stay higher for longer – 3.5% in 2025, 2.5% in 2026, returning to the 2% target in 2027.

- Interest rates are expected to fall modestly to around 3.6% in 2026 before returning towards 4% by 2030.

- The government is still meeting its fiscal rules, but only due to tax rises, not improved growth.

Inheritance Tax and Succession

No change to the key headlines from last year:

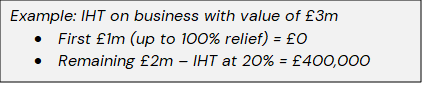

- Cap imposed on relief available under Agricultural Property Relief (APR) and Business Property Relief (BPR). First £1m of combined business and agricultural assets remain exempt.

- For assets over £1m – Inheritance Tax (IHT) will be applied at 50% of the full rate (i.e. 20% effective rate).

New changes announced:

- The £1m APR/BPR allowance will be transferable between spouses/civil partners.

-

- Any unused allowance on first death can be used on the second – including where the first death occurred before 6 April 2026.

-

- The IHT nil-rate band (£325k) and residence nil-rate band (up to £175k) have both been frozen until April 2031, one year longer than previously planned.

The APR/BPR reforms will fundamentally change the inheritance position for farming families – now is the right time to review your position. The new transferability gives spouses more flexibility, but does not remove the need to restructure ownership intelligently. You should review wills, partnership agreements and asset valuations now, not after the reforms take effect.

Personal Taxes and Wealth

- Income Tax and National Insurance thresholds freeze to be extended until April 2031.

- Income Tax thresholds do not directly apply to Scotland as Income Tax is a devolved matter, but the freeze to the personal allowance and NIC thresholds will apply.

- While a small announcement, this is one of the largest impact items in the budget – raising an extra £8.3bn a year.

- 2% tax rate increase on dividends and savings income.

- Cash ISA limit reduced to £12,000 from 6 April 2027 (within an unchanged overall £20,000 ISA allowance) to encourage investment in stocks and shares.

- Over-65s exempt – retain the full £20,000 cash ISA allowance

- Removal of the 2-child benefit cap in Universal Credit and Child Tax Credit from 2027

- From 6 April 2029, salary-sacrificed pension contributions above £2,000 per year per employee will be subject to both employer and employee National Insurance Contributions (NICs).

Partners, company directors and landlords will pay more tax on drawings and investment income, reducing disposable cash available for family or business reinvestment.

Farms operating through companies may need to reassess remuneration strategies — dividends, salaries, bonuses, and pension contributions all interact differently under new rules. If you operate a company, the pension salary-sacrifice cap means you should adjust longer-term pension planning now to avoid unexpected NIC costs from 2029.

Capital Allowances and Investment

Most farm machinery investment will continue to fall within existing reliefs:Annual Investment Allowance (AIA) – 100% relief on up to £1m of qualifying plant and machinery for all business types.

- Full expensing – remains available to companies for qualifying new main-rate plant and machinery.

However, two important changes affect expenditure outside AIA/full expensing:

- Main rate Writing Down Allowance reduced from 18% to 14% (from April 2026), slowing the rate at which tax relief is given. This means businesses will claim a smaller annual deduction on the tax value of qualifying plant and machinery.

- New 40% First-Year Allowance (FYA) (from 1 January 2026)

-

- For investment in new main-rate assets that don’t qualify for full expensing or not covered by AIA.

-

- Remaining value written down at 14% thereafter.

Farms planning major capital investment (new machinery, buildings, equipment) should review timing carefully, as bringing forward certain purchases into 2026 could secure the higher 40% year-one relief where it applies.

Employment Costs

Increase in National Minimum Wage and National Living Wage:

When compared to 2024 rates (£11.44 and £8.60 respectively) this represents an 11.1% increase for 21 and over workers and a 26.2% increase for 18–20-year-old workers. This will make a significant difference for industries with high levels of employees that are paid close to the National Living Wage such as dairy, pigs, poultry or fruit/veg businesses. Labour-intensive sectors should budget now for the increases in staff costs.

Other notable points

- From April 2027, the government intends to raise fuel duty (currently 52.95p per litre) in line with inflation, along with gradually unwinding the temporary 5p cut by March 2027.

- A new Electric Vehicle Excise Duty (eVED) regime from April 2028 will introduce “pay-per-mile” taxation for electric and plug-in hybrid cars.

- From April 2027, HMRC will roll out “digital prompts” in VAT filing software, nudging businesses about anomalies at the point of filing.

- From April 2029, all VAT invoices will have to be issued in a specified electronic format – effectively mandatory e-invoicing for VAT-registered businesses. An implementation roadmap will be developed with stakeholders and published at Budget 2026.

If you’d like to discuss what these changes mean for your farm or croft, speak to your local SAC Consulting adviser for guidance.

Andrew Coalter, Senior Agricultural Consultant and Area Manager, Andrew.Coalter@sac.co.uk

Posted by SAC Consulting on 11/12/2025